- Payments & Point of Sale Solutions

The Future of Payments: Zeller's Take on Emerging Trends

As the world of payments continues to evolve at a rapid pace, businesses need to stay ahead of the curve to ensure they are providing the best possible experience for their customers.

Cash has been on a well-documented decline since the mid-2000s, which was accelerated by the COVID pandemic. At Zeller, we design and build payment and financial solutions to meet the changing needs of business owners at any stage of their journey. We spoke to Zeller's Head of Product, James Vatiliotis, about the payment trends that we see shaping business in 2023 and beyond.

Industry-specific payment solutions

One-size-fits-all payment solutions are becoming a thing of the past. Industry-specific solutions are gaining traction because they provide products tailored to the unique needs of different businesses. An example is Pay at Table for the hospitality industry. By allowing customers to pay at their table, busy restaurants are able to turn over tables more quickly resulting in increased revenue, whilst also reducing bottlenecks at the point-of-sale system with many customers wanting to pay at once.

Surcharging is helping to offset rising economic costs

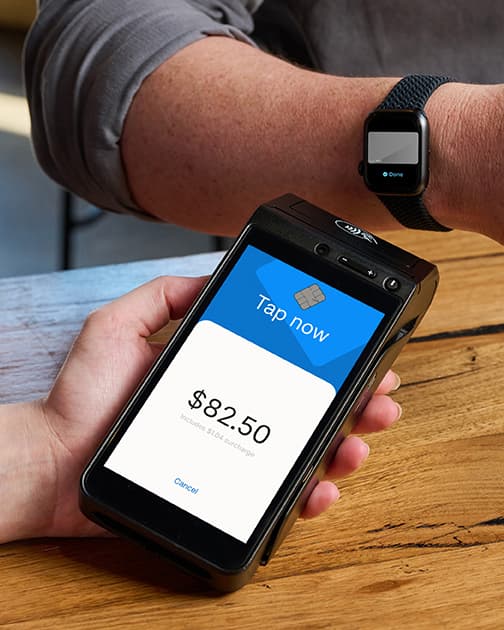

Across the board, we are seeing an increasing number of merchants choosing to pass on the cost of their EFTPOS processing fees to their customers. Although surcharging is divisive, there is an argument to say that it provides a degree of transparency. For business owners facing increasing operating costs, surcharging provides a flexible option to reduce expenses. Ultimately all costs incurred by businesses need to be recouped in their pricing, so whether it's blended into the cost of the item or added as a surcharge the result is the same. Big businesses like Aldi have been applying surcharges for years, so Australian consumers have become increasingly familiar with the practice. It is a commonly used feature of Zeller Terminal, however, you can choose to use it, switch it on and off as it suits, or surcharge only part of the transaction fee.

Accepting card payments in more ways than ever

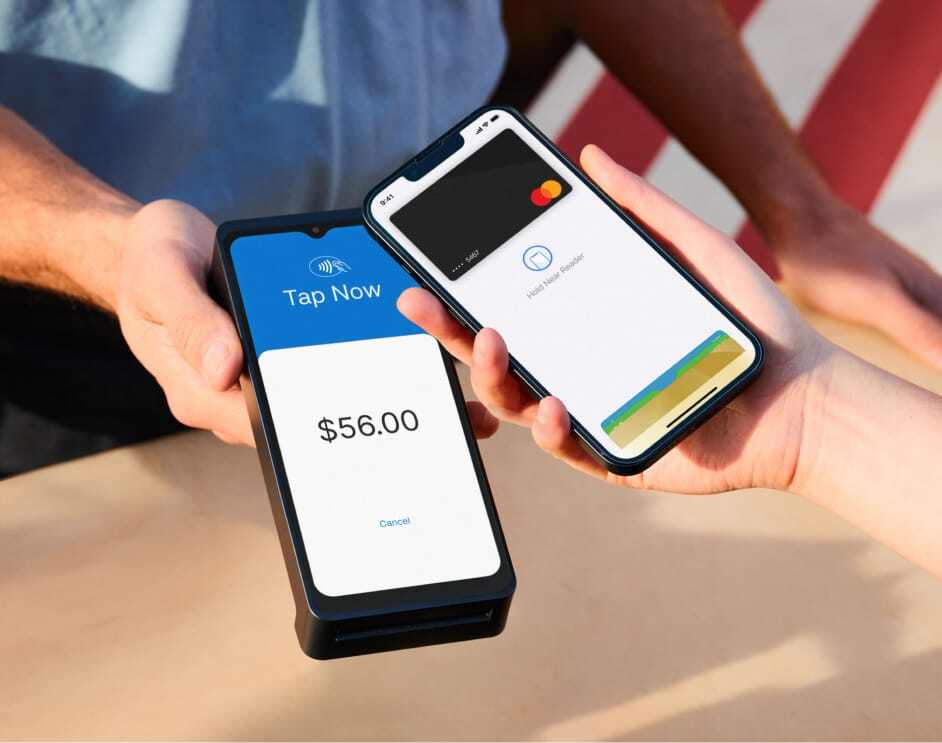

The launch of contactless payments on commercial devices like tablets and smartphones (CPoC standard) is a game-changer. Soon, merchants will simply have to hold out their phones and invite customers to tap their physical or virtual cards to process a payment. This is just the beginning of a new wave of payment innovation, and we're sure to see mobile kiosks, point-of-sale tablets, and a number of other devices follow.

Wallets may soon be a thing of the past

Mobile wallet transactions make up over 25% of in-person payments in Australia. With Medicare already cardless, cash acceptance declining and some states launching digital licenses, soon there may not be a need to take a wallet at all. We have witnessed this trend in our own product suite, with virtual Zeller Debit Cards making up approximately 50% of all cards created by our merchants. Our virtual cards can be created on the Zeller App or Zeller Dashboard and added to your digital wallet in minutes, ready to be used.

The NPP has proven its abilities

Since launching in 2018, the New Payments Platform (NPP) has over 90 million customer accounts processing more than $1 billion. The NPP is open access infrastructure for fast payments in Australia – the platform enables innovation by fintechs and other companies building on top of this network. The introduction and uptake of the NPP means that Australia is unlikely to see the introduction of a closed network payment system like WeChat and Alipay. This is not to say these products definitely won’t have uptake in Australia, but their value proposition would need to be more than real-time money movement – since this is possible through the NPP.

We are always keeping an eye on emerging trends in payments to ensure Zeller provides the best possible solutions for every business. It is exciting to compare the payments landscape in Australia to what it was ten years ago and imagine how it might be in the years to come as innovation and our access to technology accelerates.

Article written by James Vatiliotis, Head of Product at Zeller