Know Your Numbers with Zeller’s Advanced Transaction Reporting and Filtering Tools

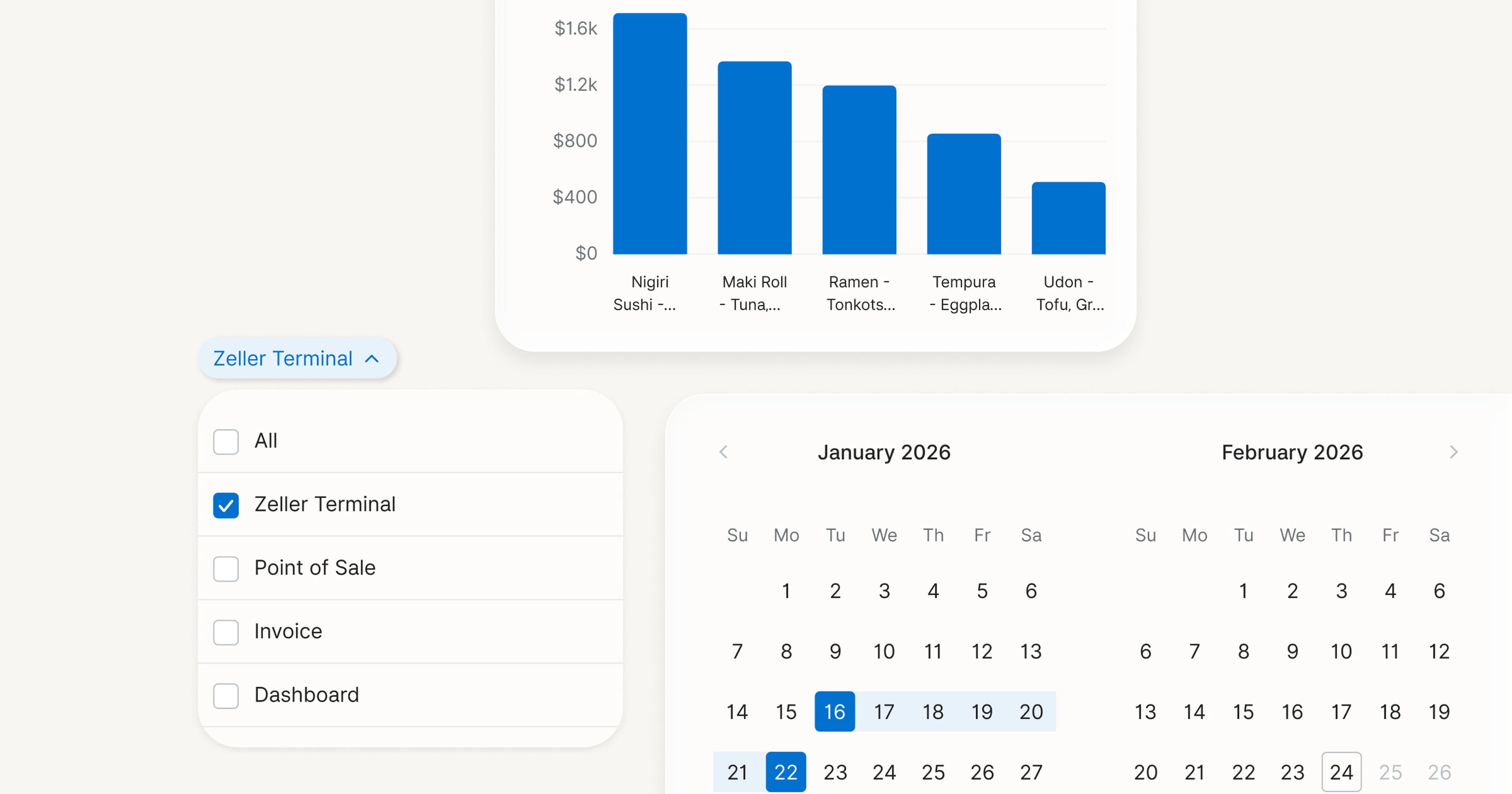

Understanding and acting on where your cash is coming from, when it arrives, and what’s driving it, is the single most important thing you can do to ensure your business success . Most point-of-sale reporting tools will let you pull a basic sales report if you’re willing to export data, open a spreadsheet, and build it yourself. Zeller is different. Whether you want to know how a product has trended season to season, which hours drive the most revenue, how a product category is performing over time, or how your quietest location stacks up against your busiest, the answer is there, in real time whenever you log in to your Zeller Account. What’s more, Zeller brings together every way that money flows in and out of your business: through EFTPOS and POS, but also invoicing, transaction accounts, transfers and debit cards. Having your cash flow all managed in one platform means less reconciliation and clearer, actionable insights. Here’s a guide to the four reporting tabs and how to get the most out of each. Your reporting hub: Zeller Dashboard Zeller Dashboard is your central hub for understanding sales performance. You’ll find reports within four different tabs — Overview, Payments, POS, and Items — each giving you a different lens on your business. Here’s how to use them. Overview The Overview tab gives you a high-level financial picture of your business. When you open Zeller Dashboard, this is where you’ll start. The Overview page is split into two subcategories: Payments and Finance. Under Payments , you can see a line graph of your total sales over time, and a breakdown of your sales (including any tips, surcharges, refunds, fees, and GST) today or this month. You’ll also find a sidebar that updates in real-time as transactions are processed. Under Finance , you’ll see the total available balance within your Zeller Transaction Account over time, a list of any other active accounts, your Zeller Debit Cards, and their most recent transactions. How you’ll use it: You own a busy lunch spot and it’s mid-morning. Before the rush hits, you open Zeller App on your phone: the overview already shows three transactions from your early-bird regulars. By the end of service you can see at a glance whether today’s sales are tracking ahead or behind the same day last week, and check your Zeller Transaction Account balance before paying a supplier invoice, all without leaving the one app. Payments Within the Payments tab you’ll be able to go deeper on your transaction history, with advanced filtering that lets you hone in on exactly what you’re looking for. Use the filters: Date — Set a custom date range, or use quick selections to see transactions from last month, last week, this month, or this week. Type — Select the transaction type you’d like to see: sales, refunds, or both. Status — Choose to see only approved or declined transactions, or both. Source — Select the payment channel the customer used: Dashboard ( payment link) , invoices , POS , terminal , or Tap to Pay . Site or Device — Choose which devices (EFTPOS terminal or your smartphone) or sites (if you manage multiple locations) you’d like to view transactions from. Crucially, the filter state is preserved as you work through your results. So if you filter to Saturday night and then change the Type to refunds, you’re still looking at Saturday night, you don’t need to reset your date range each time. Once you’ve narrowed down your results, you can export them as a CSV, PDF, or Excel (XLS) file — whatever works best for your accounting or reconciliation workflow. How you’ll use it: You manage a pub that trades from 11am to 2am. It’s Monday morning and you want to review how last Saturday night went. Set the Date filter to Saturday 11am – Sunday 2am, then set the Source filter to Terminal. In seconds you have a complete list of every card payment processed at the bar during that window. If anything looks off, switch the Status filter to show declined transactions to see whether any payments didn’t go through. POS The POS reports tab is dedicated to all sales processed through Zeller POS. It’s split into five subcategories — Summary, Sales, Categories, Items, and Sites — each giving you a clear breakdown of your sales from a different angle. Summary — A snapshot of gross sales, net sales, and average transaction value, with a graph of gross sales over time (by revenue or number of transactions), a view of how your sites are performing against each other, and a quick look at your top-selling categories and items — all filterable by date and site. Sales — Gross sales broken down by hour of the day or by day of the week, filterable by site and payment method (cash or card). Also includes a full financial summary, covering all incoming revenue and outgoing adjustments such as discounts, refunds, and service charges, plus a payment method breakdown showing the card-to-cash split. Categories — Your best and worst-performing categories at a glance, a line graph comparing how different product categories trend over time by revenue or quantity sold, and an exportable table of category sales data including totals, quantities, and share of overall revenue. Items — A snapshot of total sales, total items sold, and average items per sale. A line graph of your top-selling items over time (by revenue or quantity), plus an exportable list of every item with its full sales data. Sites — Your best and worst-performing locations at a glance, a line graph of top sites by sales over time (by revenue or quantity sold), and an exportable site comparison table. How you’ll use it: You run three cafés across the city and are trying to decide whether to extend trading hours at your quietest location. Open the POS tab and go to Sales, then filter to that site. The hourly breakdown shows a consistent drop-off after 2pm, far steeper than your other two locations. Switching to the Sites view confirms the pattern: your other two locations peak between 3pm and 5pm, while this one flatlines. That’s a clear, data-backed case for either trialling an afternoon special to drive foot traffic, or reconsidering the extended hours investment altogether. Items The Items tab is where you can drill down into the sales data of specific products or services sold through Zeller POS, POS Lite, or Zeller Invoices. At a glance, you’ll see your total revenue, total sales, and number of items sold. You’ll also find a graph of top items by revenue, and another of top items by amount sold. Below that is an exportable list of all your items, complete with variant or modifier, SKU, category, number sold, and price. How you’ll use it: You own a bottle shop and are placing your quarterly order. Open the Items tab, set the date range to the last 90 days, and sort by number sold. Your top performers jump out immediately, so you know to stock up on those. But the ‘top items by revenue’ graph tells a different story: a premium craft beer is in the top five by revenue but not by volume. That means a smaller number of customers are spending more on it, a signal it’s worth expanding your premium range, and possibly creating a dedicated section in-store to drive more of those high-value sales. Start making data-driven decisions with Zeller today Whether you're tracking a single site's daily takings or comparing performance across a national network, the data you need is organised, filterable, and exportable in just a few clicks. It's free to sign up for Zeller, so create your account today and start exploring the reports and tools available to help you manage and grow your business.