- Payments

How to Apply a Custom Surcharge with Zeller

Zeller Terminal allows businesses to apply custom surcharges to card payments.

Custom surcharges help recover processing costs fairly and transparently.

Ensure surcharge amounts comply with regulations and do not exceed actual costs.

Surcharges are automatically calculated and applied during the payment process.

Transparent surcharging improves customer trust while maintaining business profitability.

In Australia, businesses can legally charge customers a fee for processing electronic payments—this is called a surcharge. In this article, we’ll show you how to apply a surcharge to your transactions using Zeller.

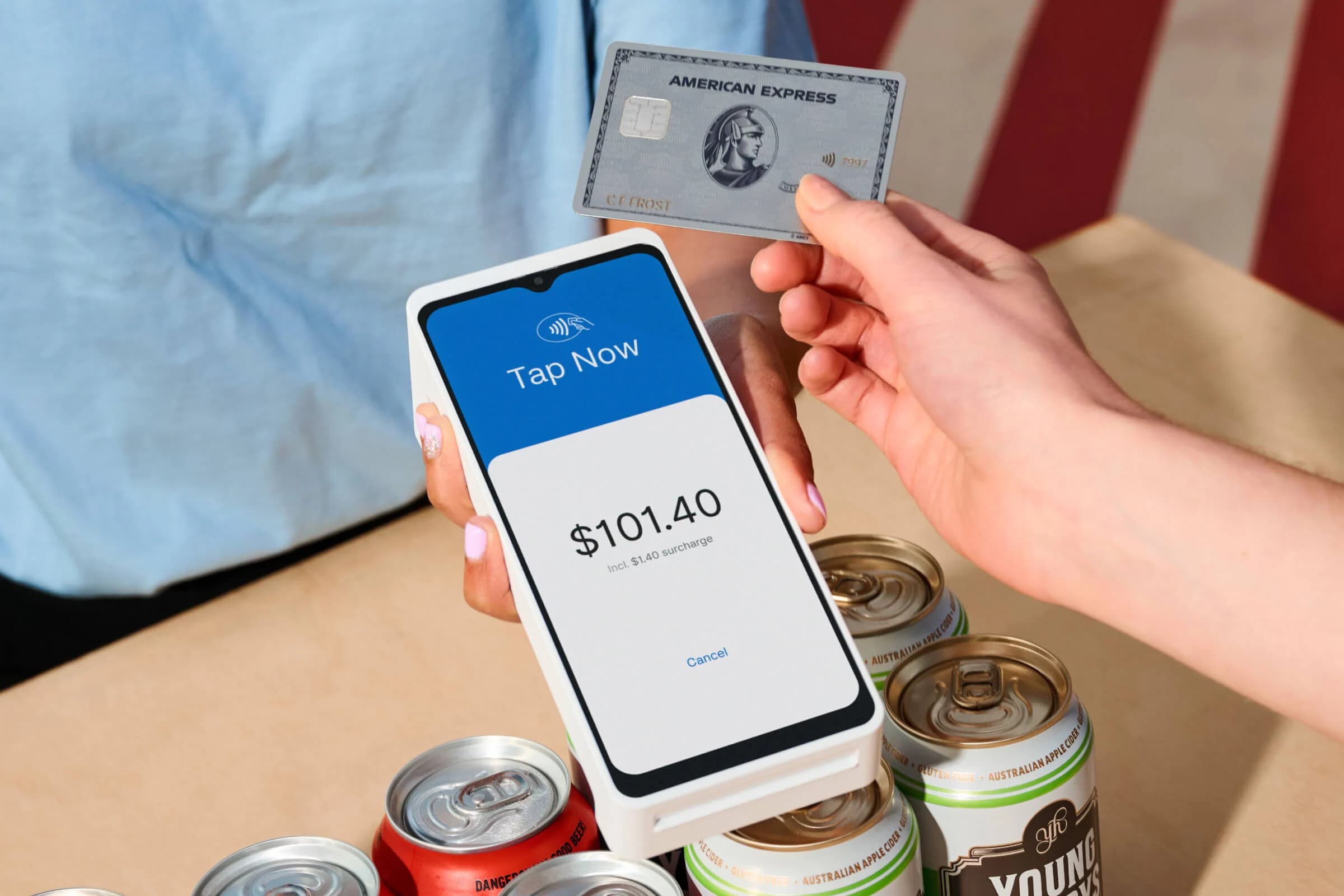

Every time your business processes a cashless transaction via an EFTPOS terminal, a small fee is charged to cover the checks and balances needed to safely move funds from a customer’s account to yours. Surcharging helps cover the cost of this fee.

Some businesses choose to absorb the fee, while others pass them on to customers. If you’re unsure whether surcharging is right for your business, check out our guide on surcharging in Australia, where we cover which industries and states surcharge the most, and the key factors to consider when deciding whether surcharging is right for your business.

With Zeller Terminal, you can easily pass on your entire transaction fee—or just a percentage—with the flick of a switch. When you pass on the full fee, your business can enjoy zero-cost EFTPOS. Keep reading to learn how.

A reminder of the surcharging rules in Australia

The ACCC enforces stringent rules to ensure businesses don’t charge more than their actual cost of processing card payments, known as the cost of acceptance. Under the Competition and Consumer Act 2010, any card payment surcharge that exceeds this cost is considered excessive and is not allowed.

Example: If your cost of acceptance for a Visa credit card is 1%, the maximum surcharge you can apply to Visa credit payments is 1%.

How much can Zeller merchants surcharge?

For in-person transactions processed through Zeller Terminal, the cost is typically 1.4% of the total transaction amount. For card-not-present transactions—such as over the phone or by mail—the cost is usually 1.7%, reflecting the extra security required to verify these payments.

The maximum surcharge you can apply is equal to your transaction fee is therefore 1.4% for in-person payments, or 1.7% for card-not-present transactions.

How to set your surcharge with Zeller

Setting your custom surcharge takes just a few moments, and can be done via Zeller Dashboard or Zeller Terminal. Simply follow the steps below, and every transaction processed through Zeller Terminal will have a surcharge applied automatically.

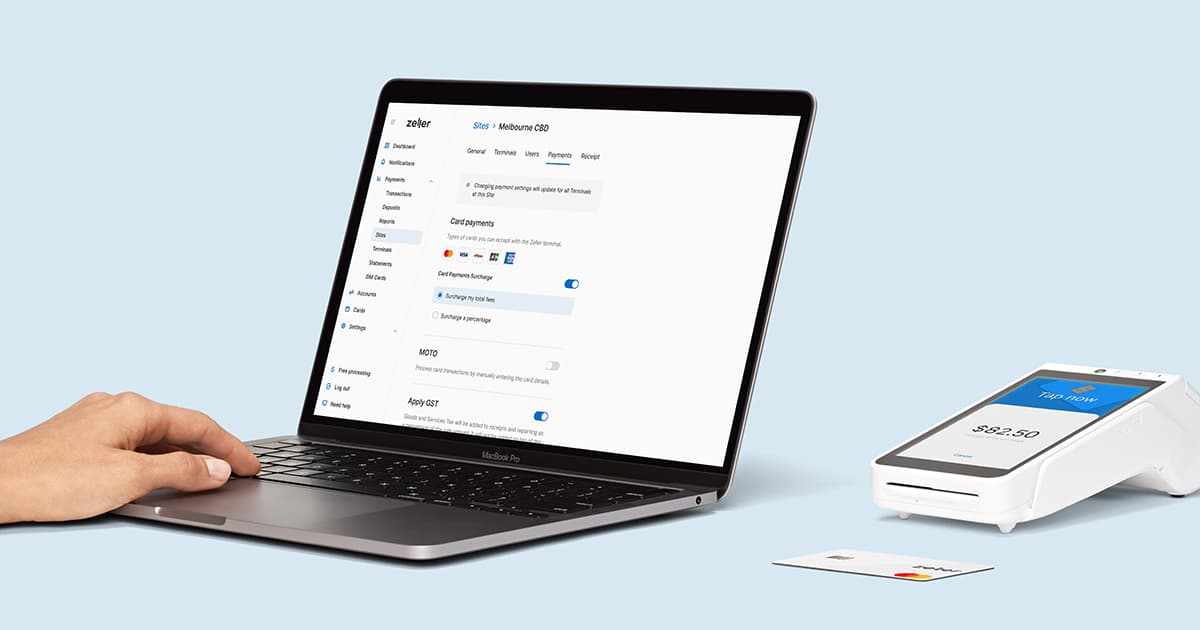

Setting your surcharge on Zeller Dashboard

Surcharging functionality can be accessed via the Payments settings for each individual Zeller Terminal.

Follow these steps to set your surcharge on Zeller Dashboard for in-person payments:

Click on the Sites tab

Select the Site you would like to manage.

Click the Payments tab at the top of the screen.

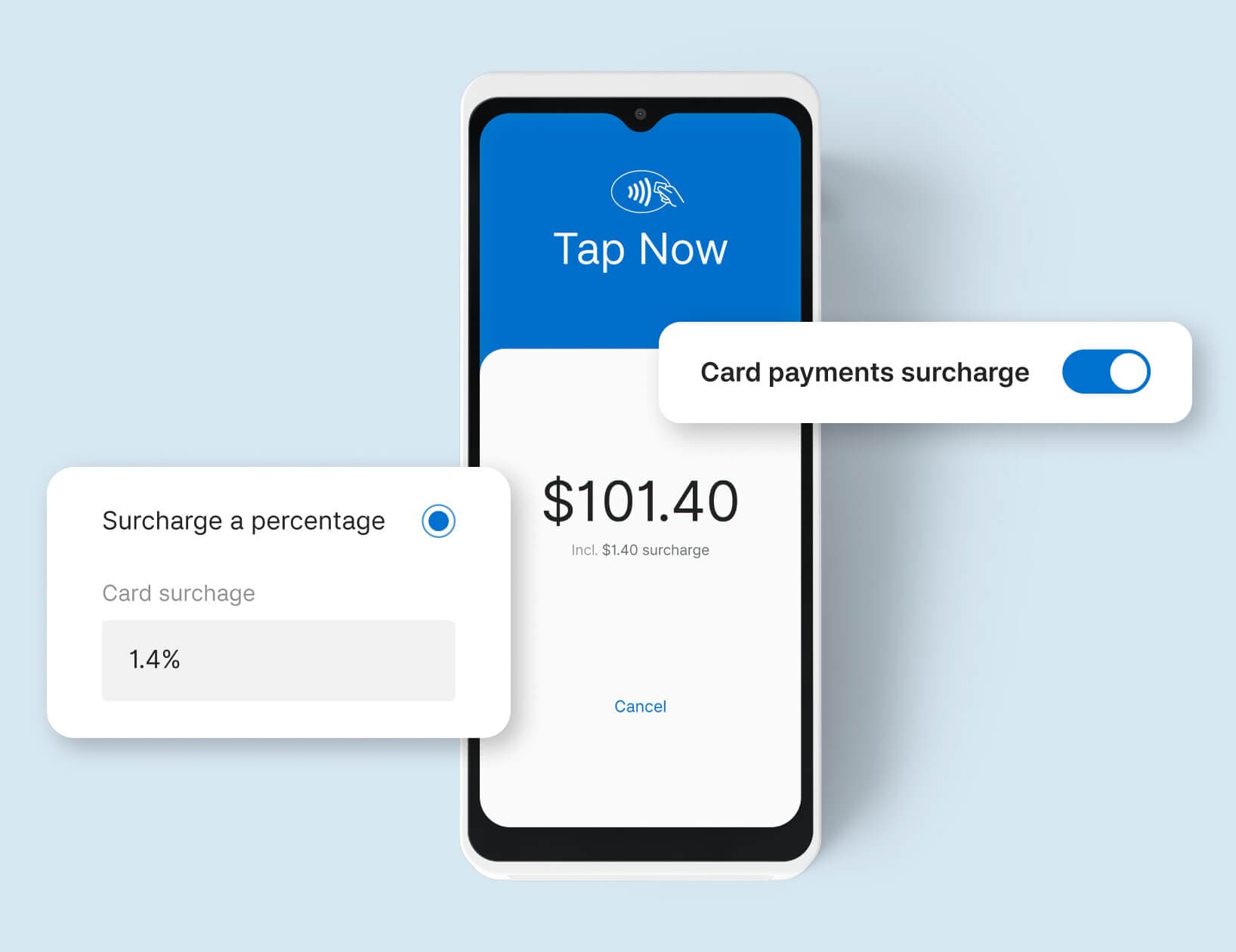

Toggle on Card Payments Surcharge

From here, you can either choose to:

Select Surcharge my total fees OR

Select Surcharge a percentage

6. Click Save to confirm your changes.

As MOTO transactions incur a higher fee, you will need to toggle on surcharging for card-not-present payments separately. You will see the option for this in the same payments tab as above. The maximum surcharge you can set for MOTO transactions is 1.7%.

Setting your surcharge on Zeller Terminal

Setting and updating your surcharge on Zeller Terminal is just as simple — however, you must be logged in as an Account Administrator. This is to protect your business from staff accidentally toggling surcharging on or off.

Confirm your device is logged in via the navigation panel

Select Settings

Tap on Site Settings

Tap on Payments

Toggle on Card Payments Surcharge

If you wish, select Surcharge a percentage

Enter in the percentage you wish to charge

For more information about surcharging with Zeller Terminal, visit the Support Centre.

Switch to fee-free EFTPOS with Zeller

Pass on your transaction costs with automated surcharging, so you'll never pay a card processing fee — no matter the card type.