- Business Growth & Optimisation

From Surviving to Thriving: A Peek Behind 4 Melbourne Businesses

Meet four Zeller merchants rebuilding their businesses in the new normal.

The outbreak of COVID-19 triggered an unprecedented disruption to business. Small businesses in Melbourne were particularly hard struck by the imposition of lockdowns and city-wide curfews. In the space of a few short months, Melbourne went from being the world’s most liveable city to the world’s most locked-down city.

Our local team took to the streets of Melbourne to discover what business looks like a few months post-lockdown. From a barbershop shuttered for 200 consecutive days, to a 143-year-old locals’ pub and a luggage brand taking the world by storm, here’s what rebuilding a business in the new normal looks like.

July

Athan Didaskalou — Co-Founder

"July is an online D2C luggage brand that was born in Australia, designed in Melbourne, and made for the world. We have one store in Melbourne CBD, soon expanding out to Sydney, and we can’t wait to take on the rest of the world as well.

We called the business 'July' for one main reason, in that it’s really fun to travel in July. People are coming back to travel, more energetic than ever to get on a plane and go and see something new, something that they haven’t seen in a couple of years.

So this ideal of travel is still stuck in their minds as something they want to achieve this year."

The Stables of Como

Luke Marshall — Manager

"The Stables of Como have been here for eight years now. We’re lucky enough to be on five acres of grounds, it means that customers can not just come here for a coffee but come here for a wedding or a birthday.

We’ve just opened a new courtyard, which has been incredibly popular with customers. Zeller is an Australian-owned and operated business. It’s incredibly easy for customers to use, and we can check real-time reporting during the day to see how we’re going.

We’ve been getting some great feedback on some changes we’ve been making in the business. We’re really focussing on what makes Como and Melbourne special. I think people are really excited to get back out there and focus on experiences."

North Port Hotel

Sean Beukes — Co-Owner

"When we first invested in the business, it was a real rundown pub. Business has changed dramatically, much like everybody else’s business has changed. You’ve got locals coming around to you and asking, 'Oh, so you’re a community pub, are you gonna stay?'

That in itself bears a lot of pressure on you to make sure that you are taking on a 143-year-old business and just going: hopefully I don’t stuff this up.

When we were approached by Zeller, I haven’t seen a banker come through here in four years since we’ve owned. I like the fact that I can call a person. We’re not owned by a major corporation. We never will be. And independent pubs are the way to go."

Smith Street Barbershop

Chris Mackertich — Senior Barber

"I guess through the last 12 months, like everywhere else in the world, we’ve been going through lockdowns and the store opening and the store closing. I think we ended up being closed for over 200 days, but it’s been good. Everyone’s been coming back into the store, everyone’s been happy to be here.

In the next 12 months I’m excited to just see the business grow and do better. We’re having some of the busiest days we’ve ever had. It’s good. It’s just good to see the business continually on an upward motion."

Supporting businesses to grow

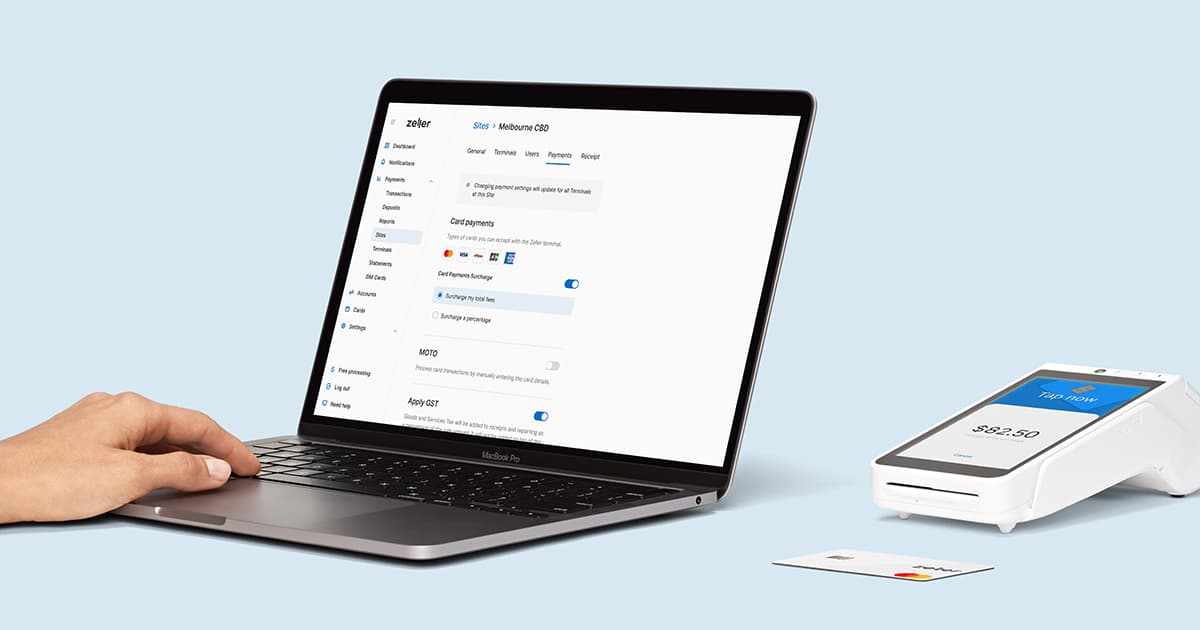

Zeller is designed for growing businesses. By giving merchants a seamless financial services solution — combining a next-gen, mobile EFTPOS terminal, free business transaction account, and free business Mastercard — Zeller significantly reduces the time businesses spend on finding a merchant services provider, completing lengthy applications, getting set up, and connecting disparate payments and financial services solutions.

Sign up online in minutes, or contact Zeller Sales for information about building a custom solution for your business.

Let us help your business grow.

Zeller Sales is here to help you succeed.

Leave your contact details and we’ll be in touch soon.

By sharing your details with us, we may contact you from time to time. We promise we won’t bug you — and you can unsubscribe from communications at any time.