Why Zeller started

Businesses deserve better.

While the disparity between the number of businesses and the limited availability of banking services to them has always been stark, the impact of the global COVID-19 pandemic amplified the importance for simpler access to smarter, integrated financial services.

Established businesses struggled, and in many cases closed their doors, as a result of stagnating cash flow. Witnessing this, it became clear to us that Zeller’s goal – to reimagine the future of business banking – is more important than ever.

What we believe

Building the future of business banking.

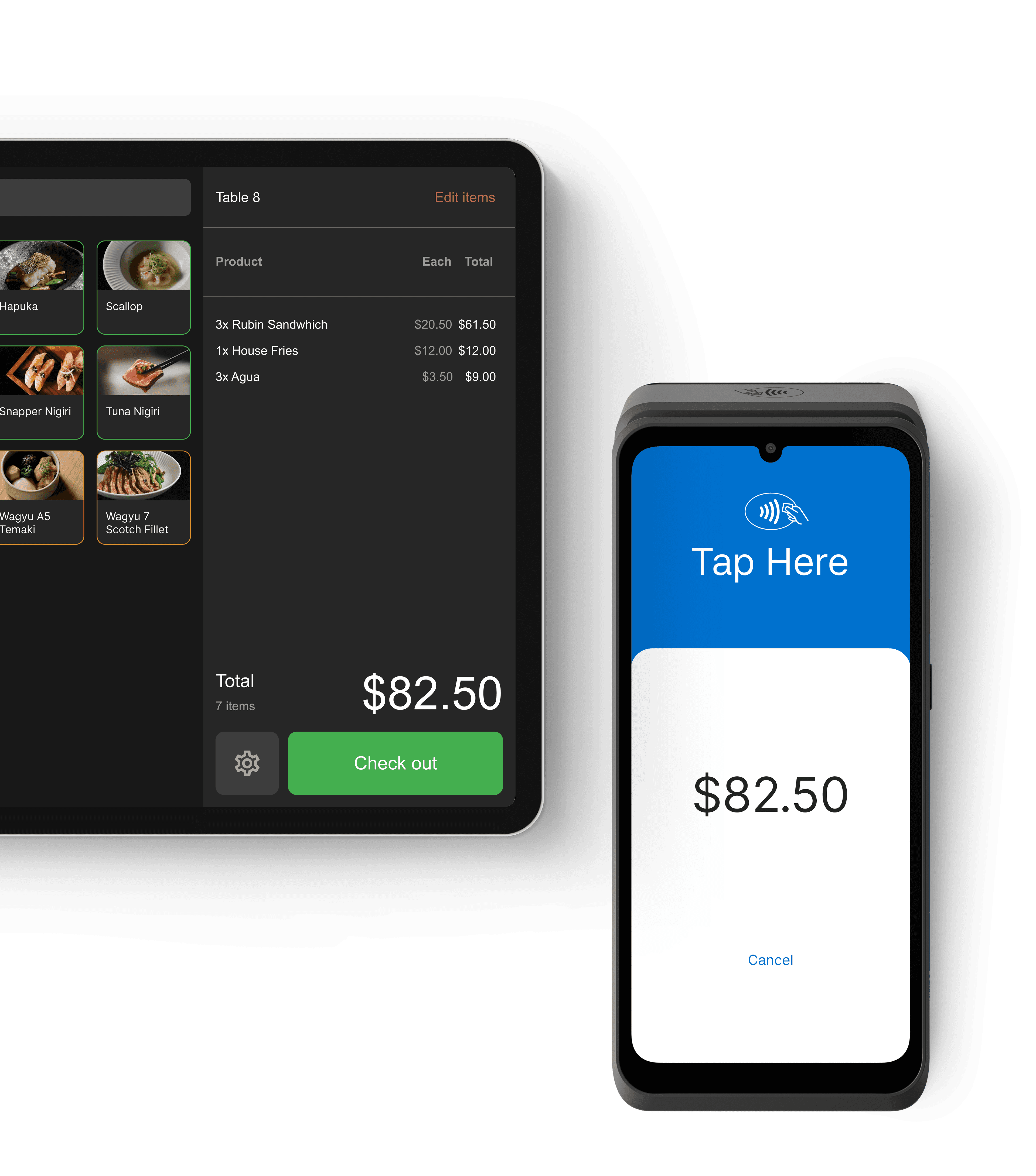

Accepting payments, managing your finances, and paying recipients should be simple. Unfortunately this isn’t always the case. Finding integrated financial solutions to help your business thrive often requires you to piece together multiple products from different providers.

With the majority of Australian businesses being underserved by the traditional banks through a lack of innovation, disconnected products, opaque pricing, and restrictive contracts, Zeller set out to level the playing field so every business can access the tools they need to manage their finances. We’re hard at work building these tools.

Discover a career with Zeller.

Join a talented team of creators, thinkers and builders who are personally and professionally invested in our mission.

Zeller is backed by leading investors.

We’re trusted by some of the world’s top investors, who share our vision of changing business banking for the better.

Support when you need it

Speak to our team

Access 24/7 human support via phone and email.

Zeller Support Centre

Search for instant answers to your questions.

Social media

Get an instant response during business hours.

Zeller Business Blog

Guides and tips to help you navigate Zeller.

It’s free to sign up for Zeller.

Create an account.

Signing up for Zeller takes minutes for most businesses, and it’s free.

Add an opening balance.

Add funds to your Zeller Account to create an opening balance.

Explore Zeller products.

Choose which payments or financial products you need for your business.

What’s new on the Zeller Business Blog

Read more on the Zeller Business Blog

Zeller Australia

ABN 14 649 001 383

Postal Address

PO Box 18238

Collins St East VIC

Australia 8003